Catch-Weight + Inverse BOM 101: Why Meat Processors Lose Margin Without Them

TL;DR: Meat processors don't sell what they make in fixed units. They sell variable-weight cuts derived from whole animals. Two ERP concepts make this work: catch-weight, which lets you track and price each piece by its actual weight, and inverse BOM, which models the reality that one input (a carcass) yields many outputs (cuts, trim, bones, fat). Without both, processors lose visibility into yield, mis-cost their products, and leave margin on the cutting floor. inecta Food ERP is built natively for catch-weight and inverse BOM, so every cut is tracked, costed, and traceable from animal to invoice.

The problem: meat doesn't behave like other inventory

In most industries, a unit is a unit. A bolt weighs what a bolt weighs. A bottle of shampoo holds 12 ounces, every time. Inventory systems built for those industries assume one SKU equals one consistent quantity, and they break the moment you put a side of beef on the cutting table.

Meat processing inverts the standard manufacturing model in two fundamental ways:

- Every piece is a different weight. A boxed ribeye is sold by the pound, not by the unit. Two cases of the same SKU can weigh different amounts. Pricing, invoicing, and inventory all have to follow the actual weight, not a theoretical average.

- One input becomes many outputs. You don't assemble a steer from parts. You break one down into dozens of products simultaneously. A single primal yields steaks, roasts, trim, bones, fat, and offal, each with its own value, its own destination, and its own customer.

If your ERP can't model both of these realities natively, you end up doing what most processors do: spreadsheets, manual adjustments, and a quiet acceptance that the numbers are "close enough." For a C-suite operator, "close enough" is exactly where margin disappears.

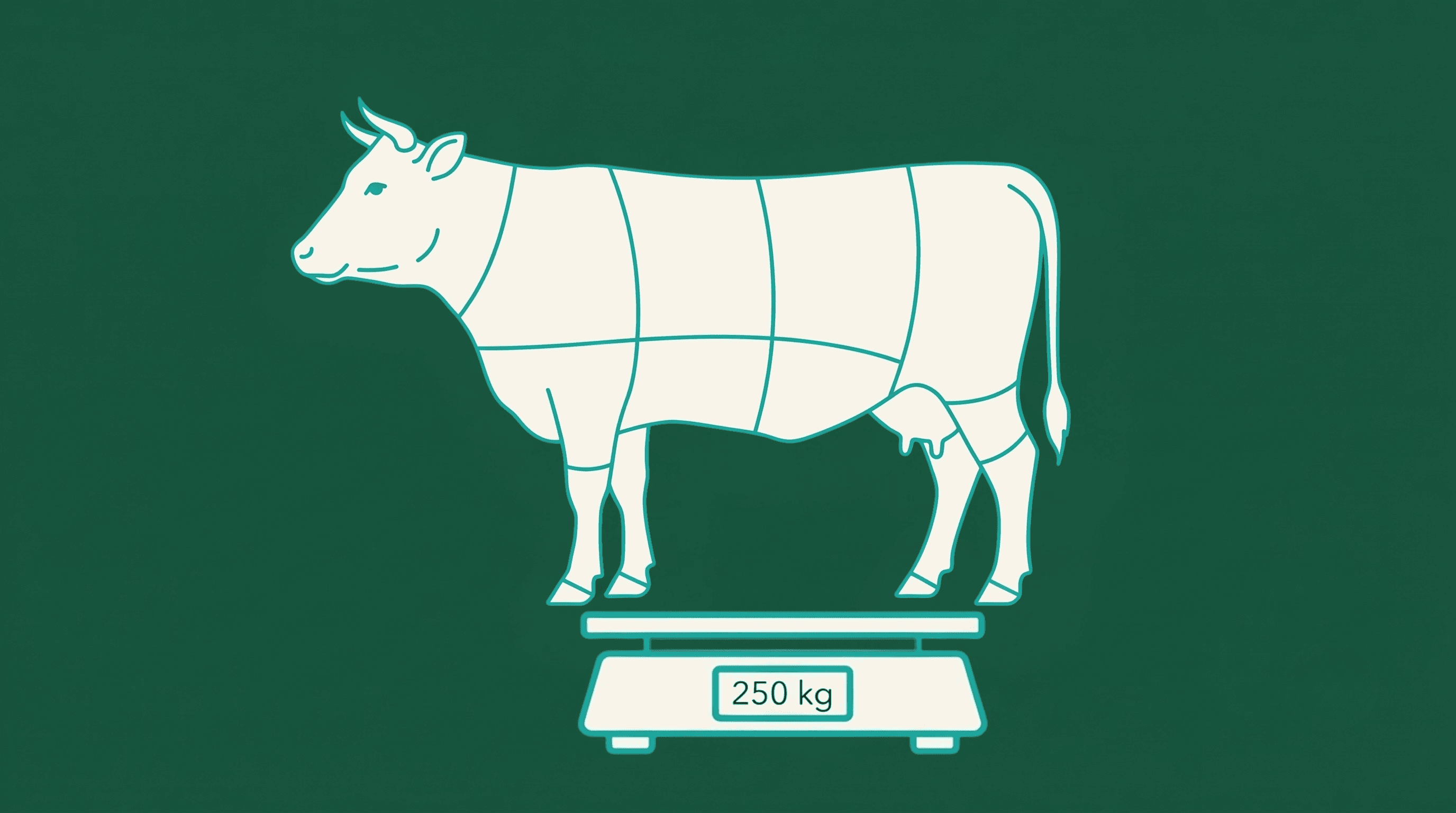

What is catch-weight?

Catch-weight (sometimes called variable-weight or dual-unit-of-measure) is the ability to track an item by two units at the same time, typically a count (cases, pieces) and a weight (pounds, kilograms).

A box of ribeyes might be one case containing ten steaks, weighing 14.3 lbs total. Tomorrow's box is one case, ten steaks, 13.7 lbs. Both are the same SKU. Both are valid inventory. The difference matters because:

- Customers are invoiced by weight, not by case. A 0.6 lb difference on a $14/lb cut is real money.

- Inventory valuation has to reflect actual weight on hand, not assumed averages.

- Pick lists, shipping documents, and EDI integrations all need to carry both units accurately.

Without catch-weight, processors either pick a fixed-weight assumption (and watch margin erode every time the actual weight is lower) or run a manual reconciliation between case counts and pound totals (and watch labor costs erode instead).

What is inverse BOM?

A standard bill of materials (BOM) lists the inputs that go into one finished product. Flour + sugar + eggs becomes a cake. The math runs forward: many components, one output.

Meat processing runs the math backward. One carcass enters the cut floor, and many finished items come out. That's an inverse BOM, sometimes called a yield BOM, disassembly BOM, or breakdown BOM.

For a beef processor, a single side might yield:

- Primal cuts (ribeye, strip loin, brisket, chuck)

- Sub-primals and portion cuts

- Ground beef and trim

- Bones, fat, and rendering material

- Offal and byproducts

Each of those outputs has a different market value, a different yield percentage, and a different customer base. The inverse BOM is what tells your ERP: when you process one side weighing 380 lbs, here is the expected distribution of outputs, here is the cost allocation across them, and here is the variance when actual yield diverges from expected.

Why catch-weight and inverse BOM have to work together

These two concepts are often discussed separately, but in a real meat operation they're inseparable. Each output of an inverse BOM is itself a catch-weight item. The 14.3-lb box of ribeyes from earlier didn't come from nowhere. It came from a primal that came from a carcass, each step tracked by actual weight.

When the two are integrated in one ERP:

- Yield is measurable in real time. You know exactly how many pounds of saleable product came out of every pound of carcass that came in.

- Costing is accurate at the cut level. Each output absorbs its share of the input cost based on weight and value, not on guesses.

- Traceability survives the breakdown. When one carcass becomes thirty products, the lot history follows every one of them, which is critical for recalls and audits.

- Margin analysis becomes possible. You can finally answer the question every meat CFO wants answered: which cuts, which suppliers, and which production days are actually making us money?

Where most ERPs fall short

Generic ERPs and even most "manufacturing" ERPs were built for forward BOMs and fixed units. Bolting catch-weight onto them after the fact usually produces one of three outcomes:

- Heavy customization that becomes fragile every time the ERP is upgraded.

- Workarounds in spreadsheets that defeat the purpose of having an ERP at all.

- A second system for the cut floor that doesn't talk to finance, leaving you reconciling two sources of truth.

For a leadership team evaluating ROI, the hidden cost of those workarounds is rarely on the original quote. It shows up later, in headcount, in audit risk, and in the margin numbers that never quite match what the floor reports.

How inecta Food ERP handles it natively

Catch-weight and inverse BOM aren't add-ons. They're foundational.

That means a single carcass receipt can flow through breakdown, packaging, and shipment with every weight captured at the source, every output costed correctly, and every lot traceable end-to-end. Your finance team sees real margins. Your operations team sees real yield. Your sales team invoices the weight that actually shipped. Your auditors see one connected system instead of a stack of reconciliations.

The bottom line for decision makers

Catch-weight and inverse BOM aren't ERP buzzwords. They're the difference between knowing your true cost per pound and guessing at it. For meat processors evaluating systems, the question isn't whether your ERP can be made to handle variable weights and disassembly. Most can, with enough effort. The question is whether it does it natively, accurately, and at the scale your operation already runs at today.

If the answer is no, the margin you're losing is bigger than the cost of switching.